Carried Away: How Low Interest Rates Shaped a Financial System, and What Happens Now

As the Federal Reserve “skipped” a rate hike last week for the first time in 15 months, the market climbed higher, signalling that investors may be starting to call the central bank’s bluff when it comes to additional hikes.

The Federal Open Market Committee may be split on future rates, but what is certain is that the financial system has already gone through a sea change, and things will be radically different from the past 20 years.

Zero interest rates: a boon to investors

Since the peak in interest rates in the 1980s, low interest rate policies have driven markets, particularly asset prices. This accelerated after the 2008 financial crisis, as central banks around the world adopted quantitative easing and zero interest rate policies (ZIRP).

“[Declining interest rates] provide a subsidy to borrowers at the expense of lenders and savers,” says Howard Marks, chairman of Oaktree Capital Management. They reduce both the cost of capital for businesses and the prospective returns investors expect, driving up asset prices.

“By simultaneously increasing asset values and reducing borrowing costs, they produce a bonanza for those who buy assets using leverage.”

During this prolonged period of ZIRP, market participants have been incentivized to invest in low-yielding projects or assets, often taking ever more risks to find yields. This makes sense: if you can borrow at 0%, any asset or project with a positive yield will be profitable, assuming the interest rate does not go up.

Carry trade: a global, systematic phenomenon

The upshot is that the entire financial system has operated as a huge carry trade.

A popular investment strategy, the carry trade often involves borrowing in a low-interest-rate currency and investing in higher-yielding assets. But it can also be applied to virtually any asset class, with investors borrowing at a low rate and generating profits from any asset class.

“The carry trade is a global phenomenon on a systematic level, encouraged by extremely low rates for an extended period of time,” says Bruce Liegel, a former macro fund manager at Millennium Partners LP and the author of Global Macro Playbook, a monthly research series on global macroeconomics at Hedder.

“This entices investors to borrow money and invest in riskier and riskier assets, with the boom in private equity and venture capital being a prime example.”

Unwinding the carry trade

This systematic borrowing at an assumed interest rate, which has now blown up, is causing financial stress for investors and asset prices, and some are starting to close out – or “unwind” – their positions.

Warren Buffett famously compared interest rates to gravity: when the force of gravity increases (interest rates go up), the prices of assets must adjust downward.

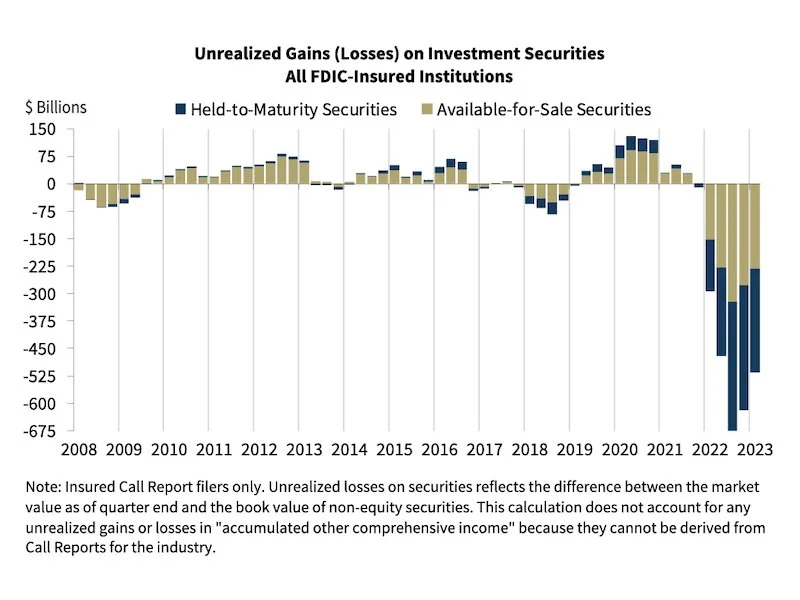

The US banking meltdown involving Silicon Valley Bank, First Republic Bank and others, is a good illustration. The banks that got into trouble invested short-term deposits in a longer-duration asset, creating a duration mismatch. With a dramatic rise in interest rates, these banks are taking large unrealized losses on these investments. They become realized when depositors take their money out, causing a liquidity issue for the banks.

Source: Quarterly Banking Profile: First Quarter 2023, FDIC

Banks aren’t the only ones

But banks are not the only players feeling the stress.

“We are also seeing it in the commercial mortgage-backed securities and real estate markets, where investors were able to borrow cheap money and invest in projects as a leveraged play,” says Liegel.

A lot of these borrowings have to be refinanced at a higher rate, and here comes the problem: investments that work in a zero-rate environment do not work in a 5% world.

A simple analogy is someone buying a vacation property with a low floating interest rate over 20 to 30 years. Now that mortgage rates have gone from under 3% to over 7%, the investment no longer makes sense and the owner may be forced to liquidate or sell, driving the asset price down in the process.

“We are starting to see a lot of this unwind from all the embedded leverages that have been put in the system over the last 15 to 20 years,” says Liegel.

A long-term trend?

But what if the rise in interest rates is just the start of a long-term trend?

In JPMorgan Chase’s CEO Letter to Shareholders, Jamie Dimon predicts that the economy will be “[heading] to higher inflation and higher interest rates than in the immediate past.”

If so, the compounding effects of the unwind could be just getting started. As central banks around the world keep interest rates high to combat inflation, the unwinding of the carry trade looks set to continue. The warning is clear: it's time to brace for impact.